The new Trump Accounts app is now available, and account funding is scheduled to begin on July 4, 2026. That makes this a good time for parents and grandparents to understand how these accounts work, where they may fit, and when another option, like a kid Roth IRA, may still be the better first choice.

What Is a Trump Account?

Trump Accounts are one of the newest savings vehicles available for children, and they have created plenty of interest among families who want to give the next generation a financial head start.

A Trump Account is a special type of traditional IRA established for the benefit of a child. The account belongs to the child, but while the child is a minor, a responsible adult manages it. The federal pilot program also provides a one-time $1,000 Treasury contribution for eligible children born from January 1, 2025, through December 31, 2028, provided the child is a U.S. citizen with a valid Social Security number. (See the IRS guidance for the full Trump Account details.)

The basic idea is simple: open a tax-advantaged investment account for a child, invest early, and let compounding do its work over time.

And that last part is where the real power is.

The Power of the Free $1,000 Seed Money

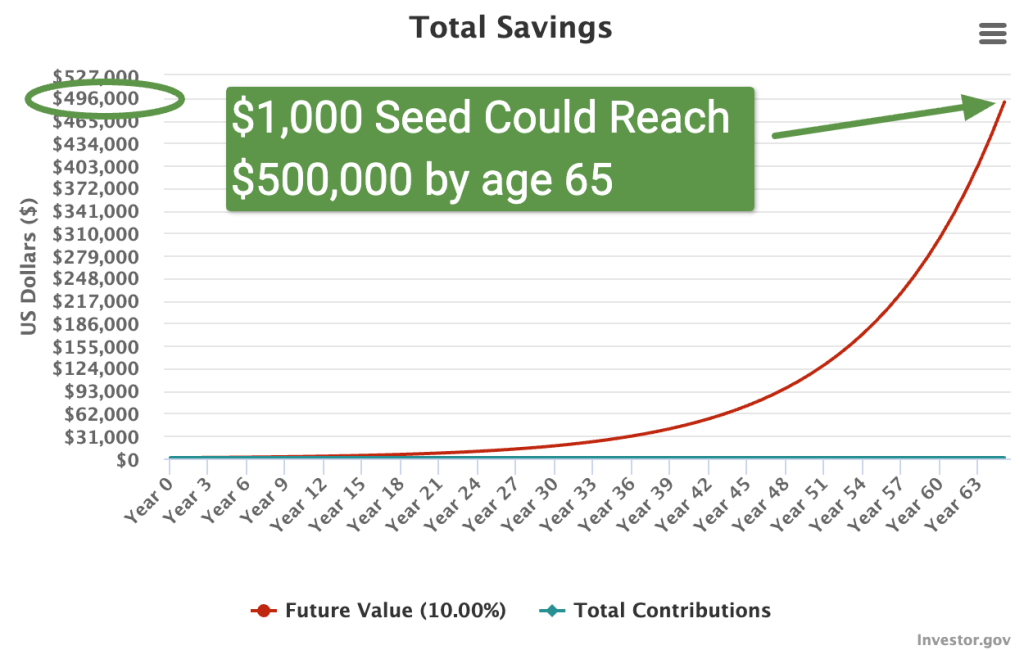

Even if a family did nothing more than open the account and receive the $1,000 government seed contribution, the long-term potential is worth understanding.

For example, if $1,000 were invested at birth and compounded at roughly the long-term historical return of the S&P 500 (10% average annual return), that single contribution could grow to nearly $500,000 by age 65. That assumes the seed money remains in the account and fully invested the entire time (and does not adjust for inflation, taxes, or future investment fees).

Of course, no one can guarantee future returns. Markets rise and fall. But this simple example shows why early investing matters so much. A small amount of money, given enough time, can become meaningful wealth.

That is the lesson I hope parents and grandparents take from this. The account itself is not magic. The magic is time, ownership, discipline, and compounding.

How to Open and Fund a Trump Account

Parents or other authorized individuals can open the account by making the proper election using IRS Form 4547 or the official online process. According to the IRS, the process requires information such as the child’s Social Security number, date of birth, and address.

Here are the basic steps:

- Confirm the child’s eligibility.

- Gather the child’s Social Security number, date of birth, and address.

- Sign in or create the required online account.

- Complete and submit Form 4547.

- Check the status of the election.

- Beginning July 4, 2026, begin funding the account if desired.

During the child’s “growth period,” contributions can generally be made even if the child does not have earned income. That is one major difference from a Roth IRA for kids, which requires the child to have taxable compensation.

Most family contributions during the growth period are subject to an annual limit (currently $5,000), so this is not an unlimited shelter. Still, for families looking to begin investing for a young child, it may be a useful tool.

The Big Limitation: Investment Choices

Here is one important downside: investment choices inside a Trump Account are limited during the growth period.

The account generally must be invested in eligible mutual funds or ETFs that track an index of primarily U.S. companies. That is not necessarily bad. In fact, a low-cost U.S. stock index fund may be a very reasonable long-term option.

But investors need to understand the tradeoff. Compared with a Roth IRA, brokerage account, or self-directed structure, Trump Accounts offer far less flexibility. You will not be able to freely choose individual stocks, crypto assets, private investments, or your own custom strategy during the growth period.

For some families, that simplicity may be a benefit. For others, it may feel too restrictive.

Why I Still Prefer the Kid Roth IRA First

From a planning standpoint, I would generally prioritize a kid Roth IRA first if the child has legitimate earned income.

Why? Because Roth investing is one of the cleanest long-term wealth-building tools available. Contributions go in after tax, the money grows tax-deferred, and qualified withdrawals in retirement can be tax-free.

Here is a simple example every parent can understand.

If a teenager contributes just $1,000 per year to a Roth IRA from ages 15 through 18 (only $4,000 total) and that money compounds at 10% annually until age 65, it could grow to more than $400,000. If that same teenager contributes $3,000 per year for those four years ($12,000 total), it could grow to more than $1.2 million by age 65. And in a Roth IRA, the money comes out tax-free.

That is the power of starting early.

This is why I love the kid Roth IRA when it is available. It teaches work, saving, investing, ownership, and long-term thinking. It also gives a young person decades of tax-deferred compounding.

But the key word is legitimate. The child must actually have earned income, and the contribution cannot exceed that income or the annual Roth IRA limit.

That is where Trump Accounts may still have a place. For younger children without earned income, a Trump Account may be one of the few tax-advantaged ways to begin investing on their behalf.

The Roth Conversion Opportunity at Age 18

One planning idea worth watching is what happens when the child turns 18.

After the growth period ends, most traditional IRA rules generally apply to the child’s Trump Account. That means the account may potentially be converted to a Roth IRA. This is where proactive tax planning becomes important.

One strategy is to convert the Trump Account to a Roth IRA once the child turns 18, using low-income years wisely. An 18-year-old may have little or no taxable income, which could create an opportunity to convert some or all of the Trump Account to a Roth IRA at a very low tax cost.

The converted amount would generally be taxable on the portion that grew in the account tax-deferred (a.k.a. the gains, not the contributions). But if the young adult has low earnings, a standard deduction, and little other income, the tax bill may be minimal, or possibly close to zero depending on the facts.

That does not mean every child should automatically convert at 18. It means families should plan ahead. Review the child’s income, tax bracket, basis in the account, education plans, and long-term goals before making a move.

My Practical Takeaway

Trump Accounts may be useful, especially for very young children who do not yet have earned income. The $1,000 federal seed contribution for eligible children is certainly worth paying attention to, and additional family contributions could help build long-term wealth.

But I would not view Trump Accounts in isolation.

If your child has earned income, look hard at a kid Roth IRA first. If your child does not have earned income, a Trump Account may be worth considering. Either way, keep investment costs low, think long term, and understand the limitations before funding the account.

The best account is not always the newest one. It is the one that fits the child’s real situation, maximizes flexibility where possible, and helps build disciplined long-term wealth.

Because in the end, this is not just about opening another account.

It is about teaching the next generation to “follow the money”, own high-quality assets, and allow time and compounding to do what they do best.