Supreme Court Upholds Health Insurance Subsidies: Here’s What You Should Know

June 27, 2015

Brandon Bourdages/ShutterstockIn the case of King v. Burwell (Case Number 14-114), petitioners argued that the language of the Affordable Care Act (ACA) specifically provides that health insurance subsidies can only be issued through state-based exchanges (also referred to as marketplaces) and not through the federal exchange. In a 6-3 decision issued June 25, the U.S. Supreme Court upheld the ACA by confirming that health insurance subsidies may also be offered through the federal exchange.

What is the issue?

A goal of the Affordable Care Act (ACA) is to provide more Americans with access to affordable health care. One of the ways the ACA attempts to make health care affordable is through federal subsidies that reduce insurance premiums and out-of-pocket costs for eligible consumers who purchase health insurance through a health insurance exchange.

At issue is a specific provision in the ACA authorizing subsidies for health-care coverage purchased “through an exchange established by the State.” The IRS has interpreted the law to include subsidies for health insurance purchased through either state-based exchanges or the federal exchange. The petitioners alleged that the IRS could not promulgate regulations to extend tax-credit subsidies to coverage purchased through exchanges established by the federal government.

What did the Court decide?

Writing for the majority, Chief Justice John Roberts acknowledged that the language of the ACA relative to exchange tax credit provisions is ambiguous. However, given the intent of the ACA as a whole, “the statutory scheme compels us to reject petitioners’ interpretation because it would destabilize the individual insurance market in any state with a Federal Exchange, and likely create the very ‘death spirals’ that Congress designed the act to avoid.”

Citing studies that suggest that eliminating the tax credits could lead to insurance premiums increasing by as much as 47%, while enrollment might decrease by upwards of 70%, Roberts opined that “it is implausible that Congress meant the act to operate in this manner.”

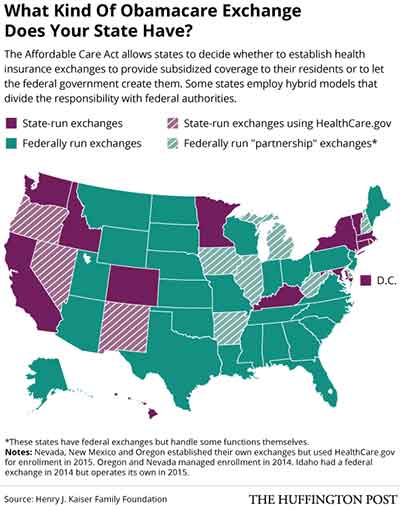

What states have their own exchanges?

As gleaned from the Court’s majority opinion, 16 states and the District of Columbia operate their own state-based exchanges.

These states include California, Colorado, Connecticut, Hawaii, Idaho, Kentucky, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, New York, Oregon, Rhode Island, Vermont, and Washington.

The federal government operates exchanges in the remaining states.

Most consumers access federal exchanges through the federal government website, www.healthcare.gov.

What if the Court ruled against the ACA?

According to the Wall Street Journal, more than 6 million people would have lost health insurance tax credits if the Court ruled against the ACA.

As of March 2015, the Department of Health and Human Services estimates that 16.4 million are covered due to the ACA.

PRAISE FOR JERRY 'S BOOK "Jerry Robinson does an excellent job of explaining the 'Petrodollar' system. His book explains exactly how this will come about, but equally important is the comprehensive section on what you can do to protect yourself."

The Strait of Hormuz is one of the most important chokepoints in the global oil market, and now it’s effectively closed in the wake of Washington’s illegal war against Iran. As it turns out, a nation that controls a strategic shipping lane just may close it if...

Topics covered on this special webcast In this live webcast, trading coach Jerry Robinson discusses the importance of analyzing monthly candlestick charts and shares dozens of monthly charts, including Bitcoin, S&P 500, gold, silver, Nvidia, and many more. Plus,...

Topics covered on this special webcast In this live webcast, Jerry Robinson analyzes the Supreme Court’s ruling against the Trump tariffs and its geopolitical and economic implications. He also explores seven key earnings reports to watch this week from stocks in his...

Please help us spread the word about FollowtheMoney.com on Facebook, Twitter, and any other social media outlets.

Silver & Gold

Call 800-247-2812 now for the best prices on gold and silver coins and receive Free Shipping and Insurance when you mention Follow the Money.

Weekly Newsletter

Stay in the loop!

Sign up today to receive our weekly e-newsletter.

Writing for the majority, Chief Justice John Roberts acknowledged that the language of the ACA relative to exchange tax credit provisions is ambiguous. However, given the intent of the ACA as a whole, “the statutory scheme compels us to reject petitioners’ interpretation because it would destabilize the individual insurance market in any state with a Federal Exchange, and likely create the very ‘death spirals’ that Congress designed the act to avoid.”

Writing for the majority, Chief Justice John Roberts acknowledged that the language of the ACA relative to exchange tax credit provisions is ambiguous. However, given the intent of the ACA as a whole, “the statutory scheme compels us to reject petitioners’ interpretation because it would destabilize the individual insurance market in any state with a Federal Exchange, and likely create the very ‘death spirals’ that Congress designed the act to avoid.”