SHOW NOTES – 1/25/14

Financial Freedom Bootcamp 2014 : Part 3

Plus, a stock investing idea from Jay Peroni, CFP

_________________________________

Don’t Put the Financial “Cart Before the Horse”

Build a Solid Financial Reserve Before Starting Investments

Last week I covered Level Two of our Five Levels of Financial Freedom. Level Two is all about protection. You must ensure that your financial assets, your income-producing ability, and your life are all protected from the unexpected. This is why insurance is such an important topic and why it is vital to structure your insurances the way you want them from the very beginning of your financial journey.

Listen to Financial Freedom Bootcamp 2014 : Part 2 >>

Today, I will cover Level Three. Level Three is all about building and diversifying your financial reserves. In Level One, you put together an emergency reserve of savings, food, water, and a Go Bag. Now, in Level Three, you will build upon this emergency reserve to create a solid financial reserve of liquid savings and food and water. Savers make better investors, so it is vital that you do not skip Level Three in order to more quickly get to the “fun part” of investing. Individuals who do not have a solid financial reserve usually choose riskier investments and put their already poor cash reserve in jeopardy. We urge you not to leap into the world of investments until you have completed Level One, Level Two, and Level Three.

Today, I will cover Level Three. Level Three is all about building and diversifying your financial reserves. In Level One, you put together an emergency reserve of savings, food, water, and a Go Bag. Now, in Level Three, you will build upon this emergency reserve to create a solid financial reserve of liquid savings and food and water. Savers make better investors, so it is vital that you do not skip Level Three in order to more quickly get to the “fun part” of investing. Individuals who do not have a solid financial reserve usually choose riskier investments and put their already poor cash reserve in jeopardy. We urge you not to leap into the world of investments until you have completed Level One, Level Two, and Level Three.

Here is a brief overview of Level Three and its components:

Build a Total of Six Months Food and Water Supply

You should already have a two month supply of food and water from Level One. Now you will increase this supply to six months worth of food and water. There are so many different ways to approach this step, and there are many gurus and experts out there now. But the way we approach this is to simply buy more of what we already enjoy eating. We do not purchase mounds of canned food and MRE’s, but instead, each time we go to the grocery store, we buy double or triple the quantities of items on our shopping list (provided they are not perishables).

Many Americans resist the idea of creating a food supply for a number of reasons. Some of the common questions that arise concerning this topic include: “How do I start my food storage?” or “What kinds of food should I store?” Others may wonder “Since I don’t cook, how do I prepare all these food items like rice, wheat and beans?” or “How do I plan a food budget for all this?” and “How do I rotate my food so it all doesn’t spoil?”

We have created a Seven Step guide to creating your six month food supply, and you can check it out here.

Water supplies are much simpler, but that doesn’t mean it’s easy. You either need to store the water in your home (which requires substantial space), or you must have a body of water nearby from which you can access water if needed. If you choose the second option, you will simply need a good portable water filter and a few storage containers.

Build a Total of Six Months Gross Income Saved

In this step, you will take your Two Months Savings Reserve from Level One and turn it into Six Months Savings Reserve (minimum). So, if you make $60,000 gross annual income, you would build $30,000 in your reserve. If you make $200,000, you would build $100,000 in your reserve. The key here is to plan for what you truly want, not for the bare minimum to get by. If you lose your job and are temporarily out of work for a few months, do you want to be forced to sell your belongings just to pay your mortgage and bills? Or do you want to have a nice cushion to bridge the gap between jobs? We like the latter scenario because, during a crisis, the last thing you want to worry about is money and how you are going to pay the bills and put food on the table.

Some other factors to consider in determining the amount of your savings reserve include your job security, the condition of your real estate, and the health of you and your dependents. You also may want to consider the amount of deductible on your auto, homeowners, and health insurances. In other words, what if you had a car accident, a house fire, and a hospital stay all the same year? It unlikely, but you don’t want to be forced to liquidate your 401(k) with penalties if you can avoid it. Naturally, such factors change with time, so it is important to review your savings reserve on a regular basis. But the bottom line is to always keep a minimum of SIX MONTHS of your annual gross income in liquid savings… and more if you have additional risk factors.

Diversify Your Six Months Liquid Savings

For the last several years, I have been explaining the importance of diversification when it comes to your finances. I believe diversification should apply to at least three separate areas of your financial life.

- Savings diversification (Diversifying your liquidity)

- Investment diversification (Diversifying your investment dollars across a wide variety of asset classes)

- Income diversification (Creating multiple streams of income into your financial life)

In the previous step, we teach the need to have six months of liquid savings at all times. However, simply having the savings is not enough. Inflation is a constant threat to your financial plan in any modern fiat monetary system. Since the U.S. government can order the Federal Reserve to print money at any time, you better believe that inflation will continue to pose a hazard to your finances. So if you want to dampen the ravaging effects of inflation that cause a loss of purchasing power on your money, diversifying your savings should be a priority. I call this strategy the Diversified Six-Month Liquid Savings strategy, in short, DSL™ Savings.

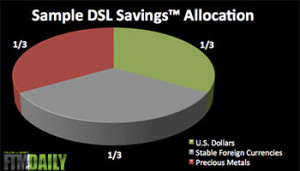

The following describes a sample DSL™ strategy. Let’s assume that you earn $30,000 per year. In order to create your DSL savings, you would need to start saving until you have a total pool of $15,000. The DSL allocation looks like this:

- One-third in U.S. dollars (i.e. savings account or money market account)

- One-third in physical precious metals (i.e. gold and silver)

- One-third in stable foreign currencies

While this is only one possible diversification strategy for your DSLTM savings reserve, I have personally found it to be particularly effective in protecting purchasing power.

Read More About Our DSL Savings Strategy >>

Update for Precious Metals Investors

Tom Cloud – Precious Metals Advisor

Tom Cloud joins us for the latest in the gold and silver markets and shares some of the fundamental and technical factors that are affecting prices right now.

Tom Cloud joins us for the latest in the gold and silver markets and shares some of the fundamental and technical factors that are affecting prices right now.

Tom Cloud:The dollar looms out there, and we’ve said many times that once it breaks back down to 78 from the 81 it is right now in the world market, that’s pretty much when we think the game is over, and that’s when gold accelerates above $2000, and then goes on up to much, much higher numbers than that. Listen to the full report.

Precious Metals Investing 101 – Free Educational Resources

Click here for access to over 10 hours of free precious metals investing educational resources >>

Trigger Trade Report

Next, Jennifer Robinson is here to update our FTM Insiders on Trigger Trading activity for the past week. We sold three positions, were stopped out of one stock, currently have one stock in play, and are awaiting the trigger price on seven stocks.

Recent Trigger Trade Performance

| Ticker | Buy Date | Buy Price | Sell Date | Sell Price | Days Held | Profit/Loss % |

| HAR | 1/13/14 | $86.03 | 1/22/14 | $90.33 | 7 |  4.99% 4.99% |

| GDX | 1/13/14 | $22.58 | 1/22/14 | $23.39 | 7 | 3.58% |

| CI | 1/14/14 | $88.67 | 1/22/14 | $90.12 | 6 | 1.63% |

View More Stock Trading Performance Results >>

INVESTING IDEA OF THE WEEK >>

Jay Peroni – Certified Financial Planner

In case you haven’t noticed, airline stocks have been red hot. With the economy improving, consumer sentiment rising, and an increase in leisure spending, the travel industry has seen a boost. The travel forecasts for the next few years looks pretty bright as well. As the economy continues to recover and consumers have more money to spend, the travel industry, especially the airlines should continue to see impressive growth. One such airline that Jay thinks has potential to grow in the coming months and years is Spirit Airlines (NASDAQ: SAVE).

In case you haven’t noticed, airline stocks have been red hot. With the economy improving, consumer sentiment rising, and an increase in leisure spending, the travel industry has seen a boost. The travel forecasts for the next few years looks pretty bright as well. As the economy continues to recover and consumers have more money to spend, the travel industry, especially the airlines should continue to see impressive growth. One such airline that Jay thinks has potential to grow in the coming months and years is Spirit Airlines (NASDAQ: SAVE).

BOTTOM LINE: Spirit Airlines (NASDAQ: SAVE) is a good buy up to $55 per share. My 12-month price target is $65-$70, representing a 30-40% potential gain from here.

Disclaimer: Investing involves risk. Always do your own due diligence and consult a trusted financial professional before making any investing or financial decisions. Jay Peroni is a Certified Financial Planner and is part of our Christian Advisor Referral. FTMDaily is affiliated with Jay Peroni and Faith Based Investor, LLC.

Recent Podcasts by Jerry Robinson

Receive our 100% FREE FTMDaily Daily News Briefing Free Right in Your Inbox

Hard-hitting news and insights that the mainstream media won’t touch >>

No spam guarantee!

DISCLAIMER: The above trading ideas are from my own personal stock watchlist and are for educational and informational purposes only. They are NOT specific buy recommendations. Trading stocks is risky and you could lose all of your money. Trade at your own risk. Jerry Robinson is not an investment advisor. You should always consult a trusted financial services professional before making any financial or investment decisions. READ FULL DISCLAIMER.