Hi Jerry. Today, I would like to focus on one of the 5 building blocks to a good financial plan that you have been teaching for sometime now and that is Building Block number 2 – protection of the assets that God entrusted to us.

Let me ask you a question, Have you ever known any one that has become impoverished as a result of going to the Nursing Home? Most people have had at least one story of someone that they know that has been devastated by the cost of going to a Nursing home.

Planning for Long Term Care is an integral part of retirement and financial planning. Long term care consists of a continuum of services including nursing home care, assisted living, home health and adult day care. The need can arise from an accident, illness or advanced age.

Statistics make a very good case for long-term care planning. For example, a 65 year old woman can expect to live another 20.1 years, and a 65 year old man can expect to live another 16.8 years according to the Commissioners 2001 Standard Ordinary Mortality Table. During these years it is estimated that the risk of entering a nursing home ranges anywhere from 20 to 49 percent.

Nursing care is expensive. Although there is a large variation from one region to another, the average nursing home cost according to the Genworth Financial 2009 Cost of Care Survey, was $74,208 per year in 2009.

There are typically five ways to protect your assets from Long-Term Care costs. For an individual with substantial retirement income and assets, self-insurance may be a realistic option. If you can’t self-insure, you could rely on the government, family or friends to help you pay the cost but all of those have major drawbacks to them. However, for those who cannot self-insure or want to rely on the government, family or friends for your long term care needs, another great option is to buy long term care insurance.

For those of you, who think Medicare is the answer to your long term care needs, let me explain how Medicare and Medicaid work. Medicare will only pay if you have first, spent at least three days in the hospital and then secondly, go to a skilled nursing facility. If you have done these two things then Medicare will pay for the first 20 days of skilled nursing care. From days 21 through 100 the patient must pay in 2010 the first $137.50 per day. If you have Medicare Supplement insurance, typically the Medicare Supplement insurance will pay the $137.50 per day through Day 100. After day 100 Medicare and your Medicare Supplement Insurance will pay nothing! Also keep in mind, Medicare does not pay for custodial care or intermediate care, only skilled care and you must be making progress or Medicare will not pay that cost. Medicaid on the other hand will pay for custodial care. However since Medicaid is a program for the impoverished, the patient must first spend down assets in order to qualify. The Medicare Spend down of assets issue is one we will explore at another time.

Private insurance is often considered by those desiring independence and choice of care and benefits to be the best option for taking care of your long term care needs and it also provides asset protection from the Medicaid spend down requirements. It is important to note that the premium for long term care insurance is going to be based on your age and the condition of your health when you apply. So obviously, the younger you are and the better your health is when you apply, will result in a lower premium.

Private insurance provides flexibility by allowing individuals to obtain care in various settings and at different care levels. Care levels include skilled nursing, intermediate care and custodial care. Contracts do not require prior hospitalization, they are guaranteed renewable and offer level premiums. You can also add coverage for home health care, assisted living and adult day care.

You can choose a daily benefit that can range from $50 to $300 or more per day and the daily benefit can be paid to you for anytime period you choose typically from 2 years through a lifetime. Benefits are paid when the insured has a cognitive impairment or is unable to perform certain activities called benefit triggers or activities of daily living. An elimination period, which is the time before the daily benefit is paid to you, will generally last from 0 to 180 days, and you can choose the elimination period. Two more riders that you can add which is of importance is waiver of premiums to limit premium costs and inflation protection to ensure that you have enough daily benefit in the future. In addition to these basic components, other benefits are often available and you can build your long term care insurance policy to be what you want it to be or what you can afford.

In closing, if you can’t self insure for long term care needs and most people can not. Then purchasing a long term care insurance policy is the best answer to help you protect all of the assets that you have worked hard to accumulate your entire life from being spent down. From my experience most people would rather that their assets went to their heirs instead of to the nursing home.

I trust this financial insight has been helpful and I look forward to the next time when I can help you provide the foundation for a lifetime of financial independence.

About John Bearss: John R. Bearss is a Retirement Specialist with the Christian Financial Advisor Network. He has been helping clients and financial professionals understand financial strategies for 24 years.

Disclaimer:John Bearss is a registered representative of and does offer securities through Sicor Securities, Inc. Lifetime Decisions Management, nor it’s representatives provide legal or tax advice. Please consult your CPA or qualified tax advisor before making any decisions. Lifetime Decisions Management, Inc. is not a subsidiary of nor controlled by SICOR Securities, Inc.

PRAISE FOR JERRY 'S BOOK "Jerry Robinson does an excellent job of explaining the 'Petrodollar' system. His book explains exactly how this will come about, but equally important is the comprehensive section on what you can do to protect yourself."

Topics covered on this special webcast In this members-only webcast, Jerry Robinson shares a sell alert on one long-term winner near all-time highs. He also analyzes the latest crypto pullback and explains why disciplined investors often find their best opportunities...

The Defiance Connective Tech ETF (UFOX) remained the #1 trend leader in our weekend ETF trend rankings for the fourth consecutive week. Our ETF Leaderboard Trend Rankings are specifically designed for trend traders who are seeking momentum trading ideas. Let’s...

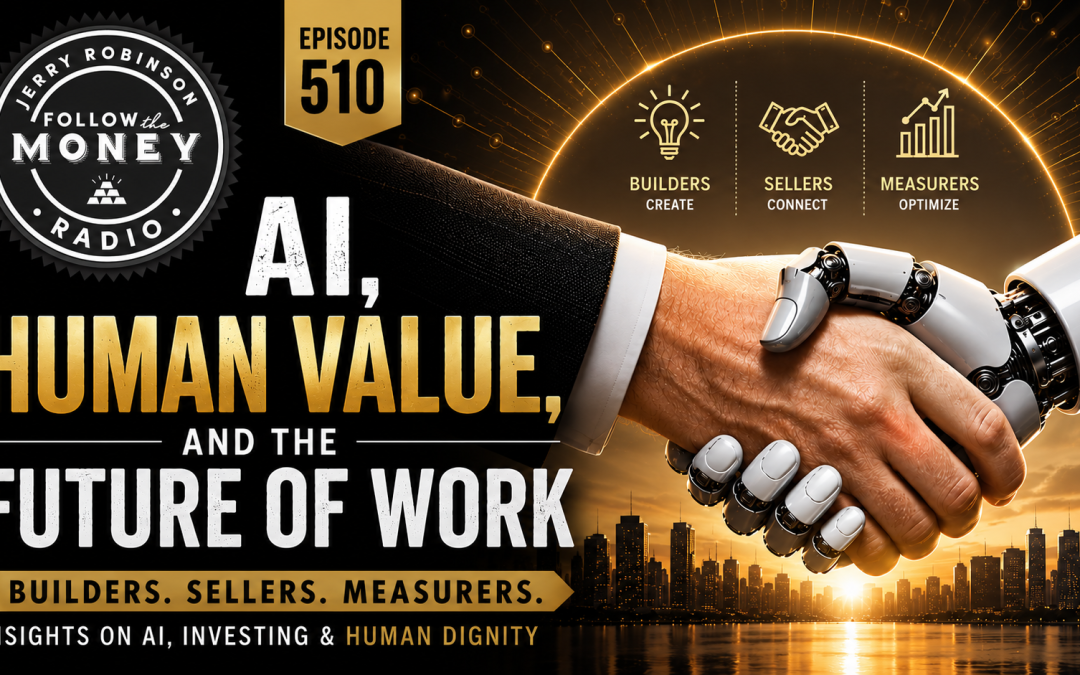

Segment 1: AI, Human Value, & The Future of Work SEGMENT BEGINS AT 02:45 Host Jerry Robinson explores how artificial intelligence is reshaping the future of work and how individuals can adapt rather than fear technological change. Topics include: Why AI may disrupt...

Please help us spread the word about FollowtheMoney.com on Facebook, Twitter, and any other social media outlets.

Silver & Gold

Call 800-247-2812 now for the best prices on gold and silver coins and receive Free Shipping and Insurance when you mention Follow the Money.

Weekly Newsletter

Stay in the loop!

Sign up today to receive our weekly e-newsletter.