by Jerry Robinson | FTMDaily Editor-in-Chief

HOUSTON, Apr 14

Yesterday, I shared with you a study on our DSL™ Savings strategy, which is short for the Diversified Six-Month Liquid Savings strategy. (You can read yesterday’s article here.) The goal of the study was to compare the returns between money saved in a regular savings account and money saved in a diversified manner according to our DSL™ Savings strategy. The study compared these two approaches over a 5 year, 10 year, and a 19 year time period. As you may recall, the difference was shocking to say the least.

|

Time Period

|

% Return on Non-diversified Savings (after inflation) |

% Return on DSL Savings™ (after inflation) |

| 2004 – 2008 |

-2.99% |

44.71% |

| 1999 – 2008 |

-0.49% |

79.31% |

| 1990 – 2008 |

13.18%

|

68.09% |

I will admit that I was completely shocked by the results. In fact, when I first saw them, I remember demanding that they be re-checked for accuracy. But sure enough, the returns were real. And while I expected my DSL™ Savings strategy system to outperform a typical savings account, I did not expect it to even outperform many investments during the same period!

Today, I am going to show you exactly how we created the above results through diversification.

I personally believe that to diversify anything properly requires that it be broken into at least three separate parts.

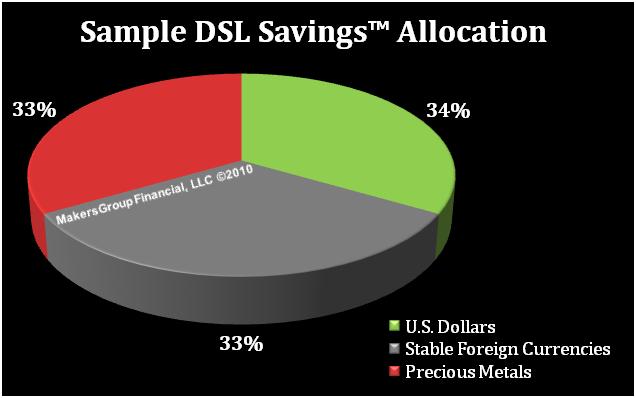

In the case of our six-month liquid savings, I hold the money in three separate areas: Stable foreign currencies, precious metals, and U.S. Dollar denominated assets.

Assuming that your 6 months of liquid savings equals $15,000, then this strategy would look something like this below.

• One-third ($5,000) in U.S. dollars (i.e. savings account, money market, cash-value life insurance, etc.)

• One-third ($5,000) in a stable foreign currency or a stable basket of currencies

• One-third ($5,000) in precious metals (i.e. gold and silver)

How We Diversified the DSL™ Savings For Our Study

For the purposes of our study, here’s how we diversified the six-month savings:

– For our one-third in U.S. Dollar denominated assets, we used 3-month T-Bills, constantly being reinvested each time they matured.

– For our one-third in Precious Metals, we divided the money into halves. One-half into physical silver bullion and one-half into physical gold bullion. (If you are wondering whether physical bullion is liquid, it is. Especially when you use a reputable precious metals dealer like we do who does not charge a sell-back fee.)

– For our one-third in Foreign Currencies, we used three different ones from 1990 until 2002. These were the Swiss Franc, the Canadian Dollar, and the Australian Dollar. Then from 2002 to 2008, we added a fourth currency: the Euro.

And that’s it. No secrets, no magic tricks, and no late-night infomercial gimmicks (although that last one would have been fun.)

Just plain vanilla diversification.

Isn’t it amazing how just a little bit of diversification can make such a big difference!

By now, I am sure many of you have questions. So tomorrow, I am going to begin explaining some of my favorite ways to diversify each of these specific areas and how to go about doing it. Tomorrow, I will start with the U.S. Dollar denominated segment. Where are some “good” and “not-so-good” places to store this one-third of your DSL™ Savings reserve today? I will be back tomorrow with some ideas on that topic.

Here at FTMDaily.com, we are working hard to create solutions for you during these difficult times of economic crisis. We invite your feedback and comments on how we may serve you better.

Until tomorrow,

Jerry Robinson – FTMDaily.com