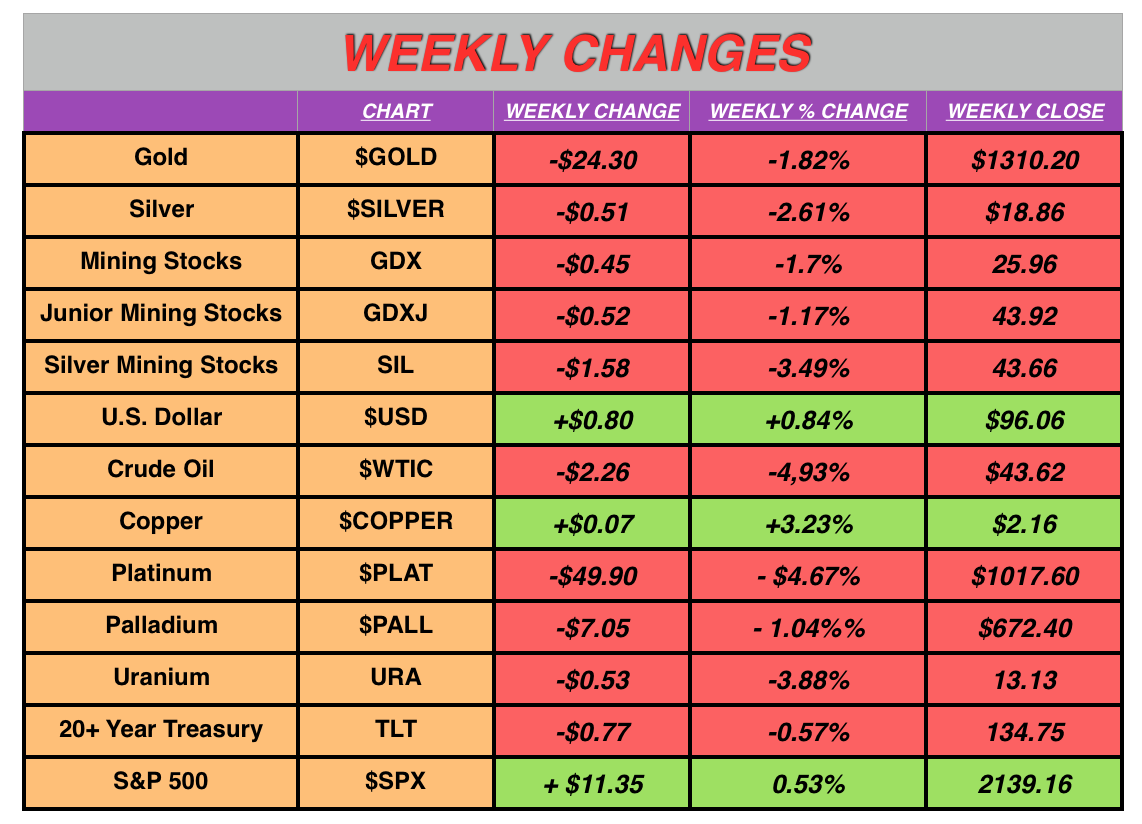

The metals traded lower this week, once again testing support near $1308 / $18.50 and are in clear short-term downtrends. Gold has closed lower 7/8 previous trading sessions and silver 6/8. The only bright spot in the metals complex this week was a rallying copper price, which tends to benefit silver.

Once again the dollar rally corresponded with a rise in treasury yields. Recent Treasuries held in Custody (TIC)data showed foreign central banks selling U.S. debt at a record pace. If this trend persists, it will leave the Fed as the “buyer of last resort.” The U.S. simply cannot afford to allow interest payments to rise. Consider that, with a $20 Trillion debt burden, each 1% rise in interest rates equates to an additional $200 Billion of interest payments annually. When rates return to levels more in alignment with historical norms, the majority of Federal tax receipts will go towards interest payments on the national debt. Contemplating the implications of that eventual reality is worth serious consideration, and there’s no time like the present to begin positioning accordingly. Here is a great place to get started.

Another wildcard for the metals will be the Bank of Japan meeting this Wednesday, which will coincide with the Federal Reserve meeting the same day. An aid to Prime Minister Abe suggested that negative rates have been beneficial [huh?], which could signal rates going even further negative.

Speculation and opinions abound as to whether the Federal Reserve will raise interest rates at their Sept 21st meeting next week, and the outcome will likely determine the short-term direction of the metals. The heavily short commercial banks would like nothing more than to see initial support levels give way.

It’s instructive to consider whose interests the Federal Reserve is actually concerned with, when considering its next move. I see several options:

The citizens. Now that is funny!

The Banks. As a private institution with shareholders and a revolving door between the banks and the Fed, they clearly have a vested interest in enacting policy that benefits their banker buddies. There’s a case to be made that slightly higher rates will benefit the “too-big-to-fail” banks in the short run.

The political establishment. A measly 0.25% rate rise has the potential to completely derail an incredibly fragile economy and stock market to the detriment of the political establishment. Personal opinion aside, Janet Yellen and company do not want a Trump presidency.

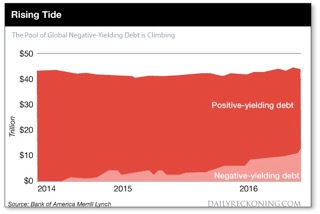

Of that “positive”-yielding debt, approx $14.5 trillion yields between 0 and 1%. About 75% of the world’s sovereign debt yields <1%. Just 6% of outstanding government bonds yield >2%

Some other entity. Although speculation, it’s entirely possible that the Federal Reserve is ultimately beholden to the World Bank, IMF, or some other global entity. After all, we know that over $16 trillion was allocated to foreign corporations and banks during the 2008 fiscal crisis. Follow the Money.

With approximately 75% of the world’s debt yielding less than 1%, it’s difficult to imagine rates going up anytime soon. In fact, it’s very possible that we will see a move towards zero or negative before any type of rate increase. The market is only pricing in a 15% likelihood of an increase next week, but is still placing the odds of a hike by December at 43%. If the Fed relents and it becomes clear that a rate hike is not forthcoming, I view that 43% as potential “fuel” for a short-covering rally in the weeks ahead, as trading positions are realigned.

Metals Related News and Trends

A whopping “2 Stars” on Amazon.

Below is a brief synopsis of several stories that highlight and expand upon some of the trends being tracked at Follow the Money.

Hostage to a Bull Market. Ken Rogoff is an influential Harvard economics professor, former chief economist at the International Monetary Fund, leading proponent of abolishing cash, and author of a newly released book titled “The Curse of Cash.” In a WSJ op-ed piece, Jim Grant systematically dismantles Rogoff’s arguments, one-by-one. If nothing else, it’s amusing to read an “economic elite” get intellectually pummeled by Mr. Grant. Eliminating cash is a precursor to negative interest rates, loss of privacy, and alone stands as valid reasoning for holding physical metals stored outside of the banking system.

Philippines to Buy Weapons From Russia and China. Until now, the outbursts of the outspoken Philippines president, who last week called president Obama a “son of a whore,” have been all talk. In an abrupt departure from his nation’s longstanding military reliance on the U.S., President Duterte said the Philippines would pursue “independent” foreign and military policies separate from U.S. interests in the region, and ordered his defense secretary to seek weapons from suppliers in China and Russia. The president also said that the Philippines would stop patrolling the South China Sea alongside the U.S. Navy,to avoid upsetting Beijing. The Philippines joins the steady flow of nations, traditionally considered “allies”, that are shifting away from the U.S. towards China and Russia. How much longer will the rest of the globe continue to save and transact in U.S. dollars, as animosity towards the U.S. mounts? Does having over 700 military installations in over 130 counties and intervention all around the globe help or hinder the world’s perception of the U.S.? The future implications of these geopolitical shifts extend beyond gold, silver, and a debased dollar.

U.S. Budget Deficit Totals $107.1 Billion in August. I want to emphasize here that there is simply no easy solution to this mess and no politician or Harvard Phd economist can change the laws of mathematics and nature. Von Mises had it right when he wrote:

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion[don’t hold your breath!], or later as a final and total catastrophe of the currency system involved.”

China and the SDR.China is the second largest economy in the world, but until now, has not been fully included with the G-20. This year China is the president of the G-20 and the recent Leaders Summit was held there. Last

China keeps several thousand tonnes of gold in a separate entity called the State Administration for Foreign Exchange (SAFE)

November the IMF made an important decision to include the Chinese yuan in the SDR valuation formula, which takes effect on 1 October. Many analysts foresee the SDR replacing the dollar as the primary pricing mechanism for global trade and as the vehicle for providing liquidity when the next financial crisis hits. Regarding Chinese gold holdings, in 2015 they announced their gold reserves had increased by 604 tonnes, rising to 1,658 tonnes. Since then, China has updated its gold reserve position monthly.These figures are deceptive, however, because China keeps several thousand tonnes of gold “off the books” in a separate entity called the State Administration for Foreign Exchange (SAFE). China will reveal their true holdings at a time that suits their strategic objectives, and when they do the price will likely soar. Until then, we can safely assume that their actual holdings are multiples higher than actually reported. The time to gain exposure is prior to any such announcement.

Saudi Arabia cannot pay its workers or bills – yet continues to fund a war in Yemen. Over 30,000 workers and many construction companies – including the Binladen group – that contract with the Saudi government have lodged complaints over unpaid wages. Low oil prices have wreaked havoc on the kingdom’s treasury, but that has not hindered deputy crown prince Mohamed bin Salman’s war in Yemen. Since the king’s favored son launched the campaign last year, aircraft flown by Saudis have bombed more hospitals and medical clinics than can be accurately tallied. The U.S. military has begun daily aerial-refueling tanker flights to support the Saudi-led coalition that is intervening in Yemen’s civil war. (Understanding Pipeline Politicsand the Petrodollar Systemwill help to decode the true nature of Middle East foreign policy.) Aside from the absolute moral repugnance of the Saudi regime, instability in Saudi Arabia equates to instability for the petrodollar system.

Jim Cook Interviews Ted Butler. This very brief written interview with silver analyst Ted Butler does an outstanding job of explaining how the silver price is set on the Commodities Exchange (COMEX) and is a worthwhile 2-minute read.

The Charts

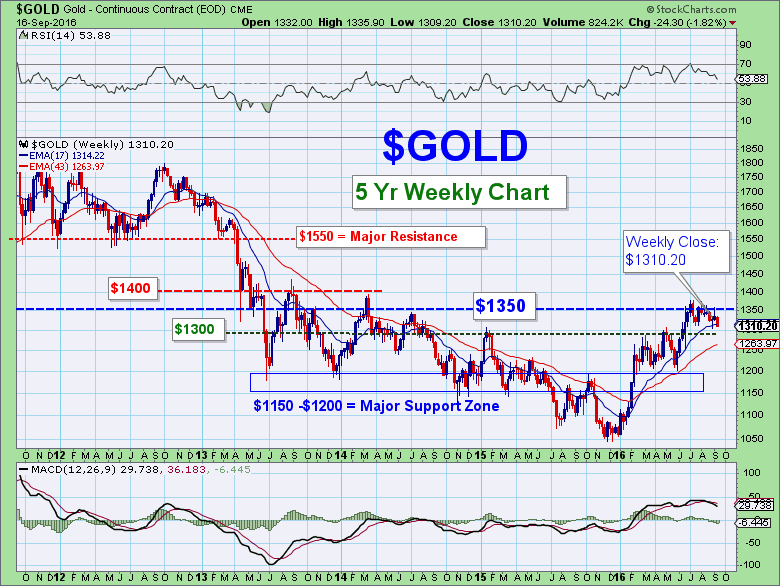

Gold

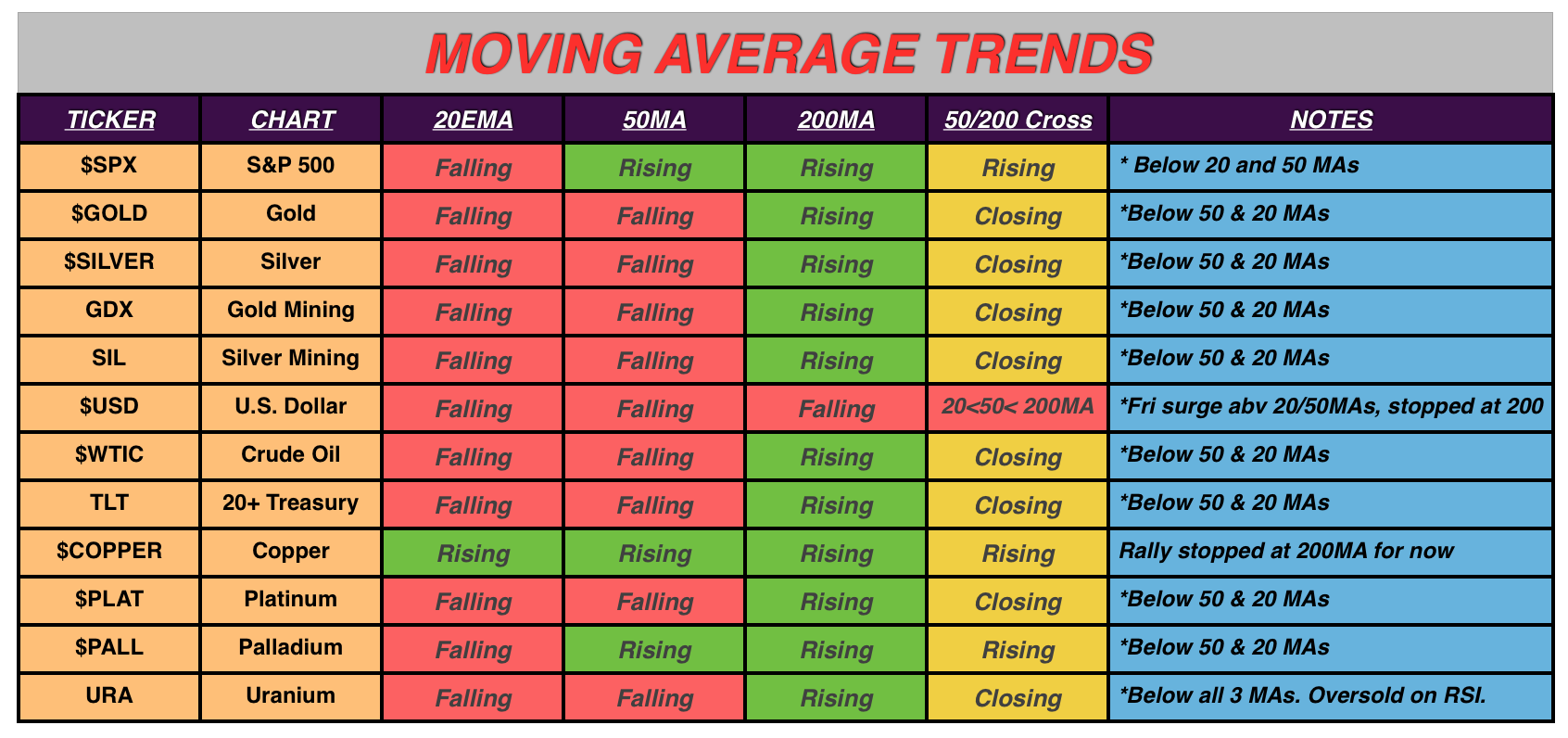

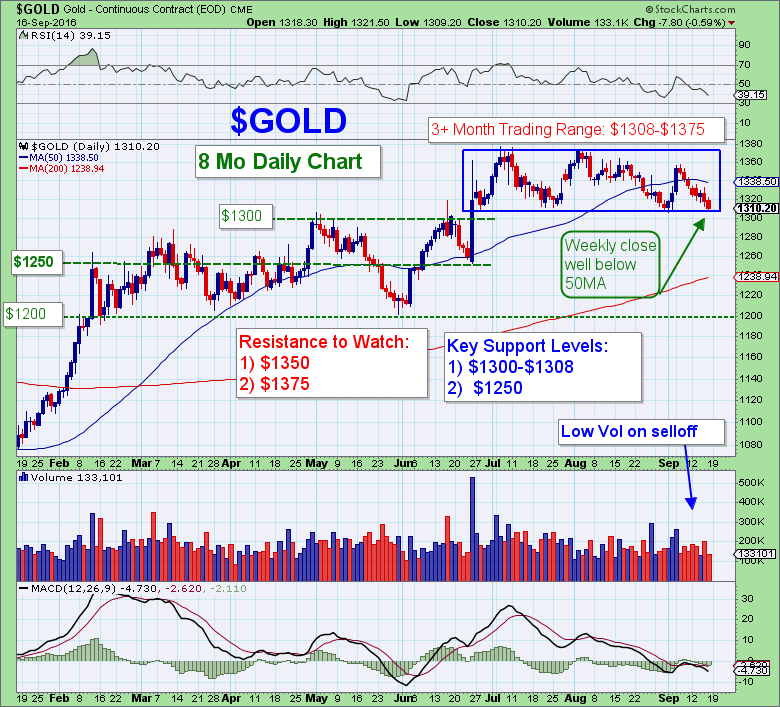

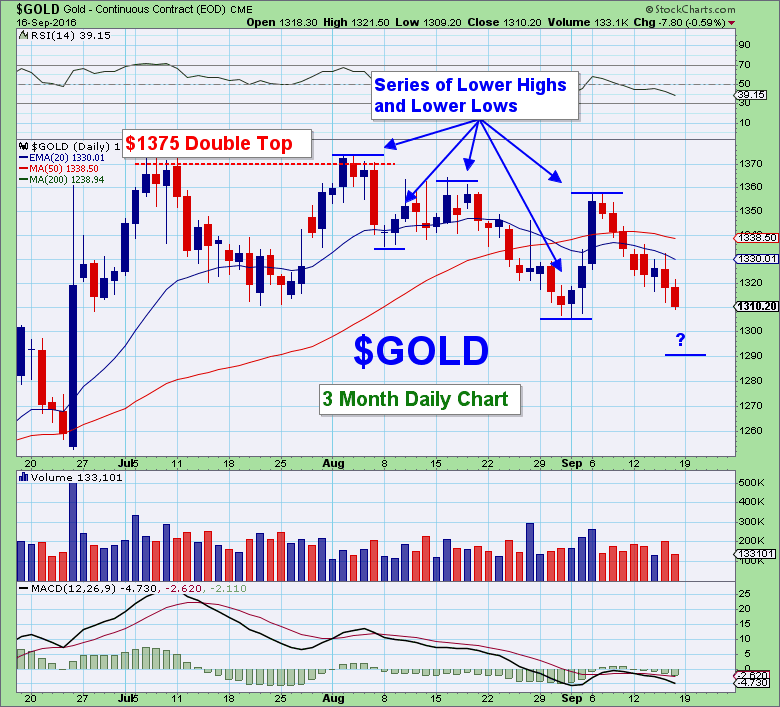

Gold once again tested the bottom of its 3-month $1308-$1375 trading range and closed below a down-sloping 50MA for the second consecutive week.

On the 3-month daily chart you can see that gold is in a clear short-term downtrend, based upon the series of lower highs and lower lows.

Selling volume has been moderate, indicating low conviction selling. It’s likely that many traders are stepping aside until this week’s Fed meeting is over.

As stated last week, position traders might consider waiting for a decisive break above or below the $1308-$1375 trading range before taking a position.

Swing traders have done well buying near the bottom of the range and selling near $1350.

For any trader or investor, the combination of Trigger Trade Proand twice weekly trading conference are a recipe for success in any market or investing timeframe. (Follow the Money has a generous promotion for the month of September.)

If $1300 gives way, look for support at $1280 and then $1250. Should the selloff persist, a rising 200MA will soon coincide with very solid support at $1250.

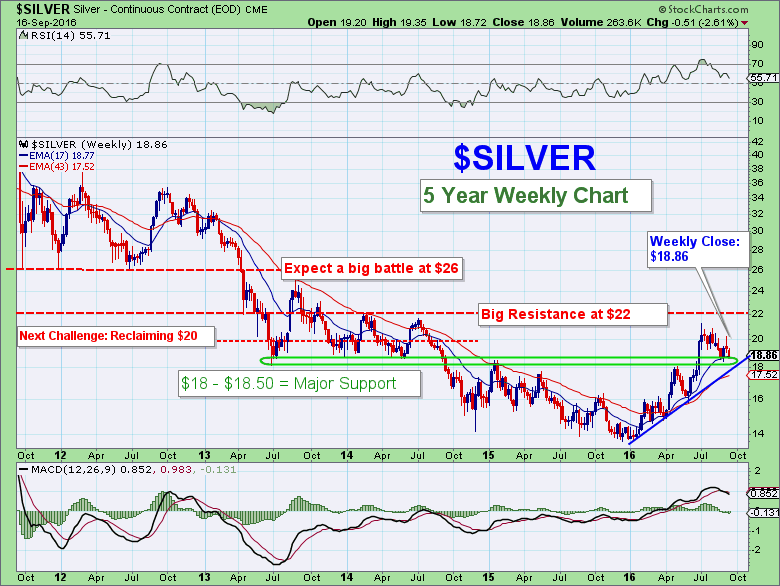

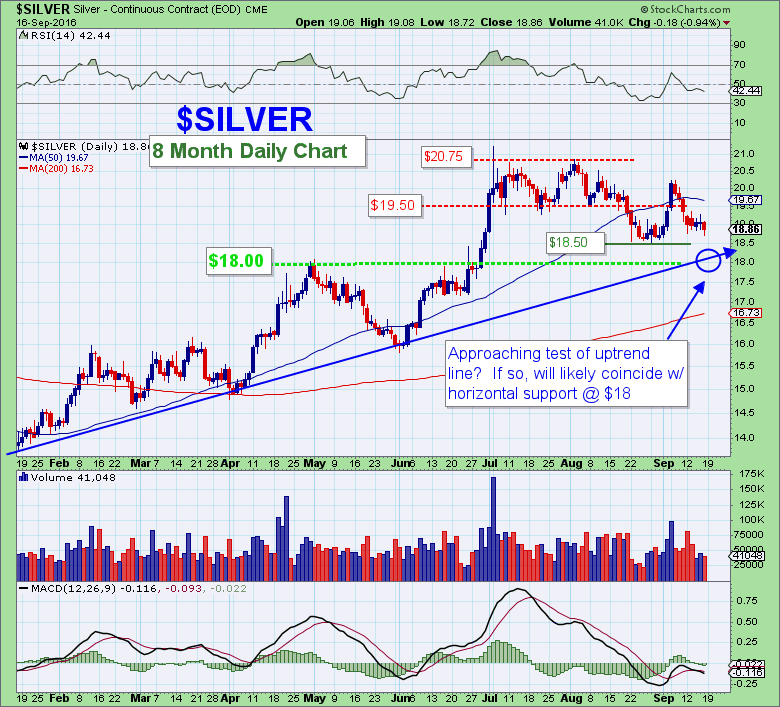

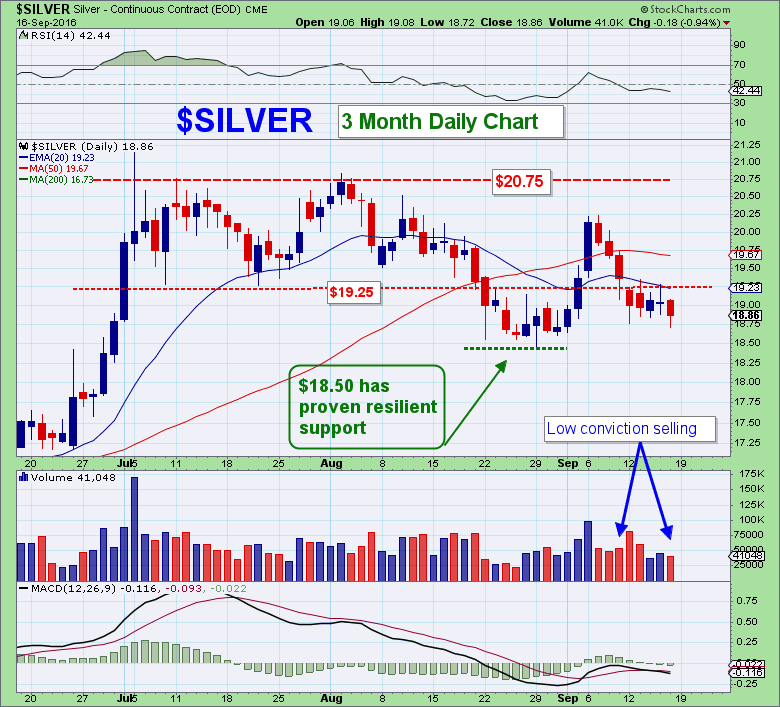

Silver

Silver closed below the $19 level and a 50MA that’s rolling over for a second consecutive week.

If $18.50 gives way, we will likely test the $18 level in short order. If so, the 200MA will coincide with the uptrend line and the $18 level by the time silver gets there. That combination makes $18 very solid support if $18.50 gives way.

On the upside, the big hurdles will be clearing $20 and the previous high of $20.75. That would set the stage for a run towards big overhead resistance at $22.

Selling volume has been light, as traders await clarity regarding the next move on interest rates. With the bank’s massively short both metals, I would not be surprised if they try to push gold and silver below their key support levels before the Fed announcement on Wednesday. If that plays out, silver could arrive somewhere near $18 in an oversold state prior to the Fed and BOJ announcements on Wed morning, leaving the metals primed for a quick bounce. That’s not a forecast, but merely a distinct possibility.

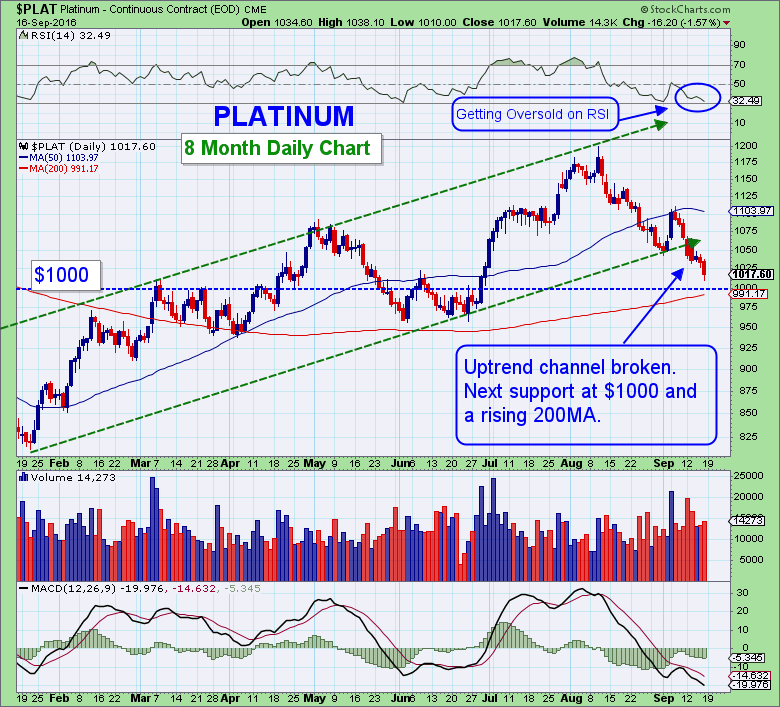

Platinum

Platinum broke below its uptrend channel and is fast approaching solid support at $1000. Just below $1000 is a rising 200MA at $991.17.

With platinum getting quite oversold on its RSI, look for a bounce off $1000 support. If that occurs and platinum can quickly retake its 50MA, it will again be in a bullish posture and poised to resume its advance.

Should the 200MA give way, it would be prescient to await signs of the uptrend resuming prior to risking hard-earned capital.

Platinum is historically undervalued relative to gold, and will likely outperform when the uptrend resumes.

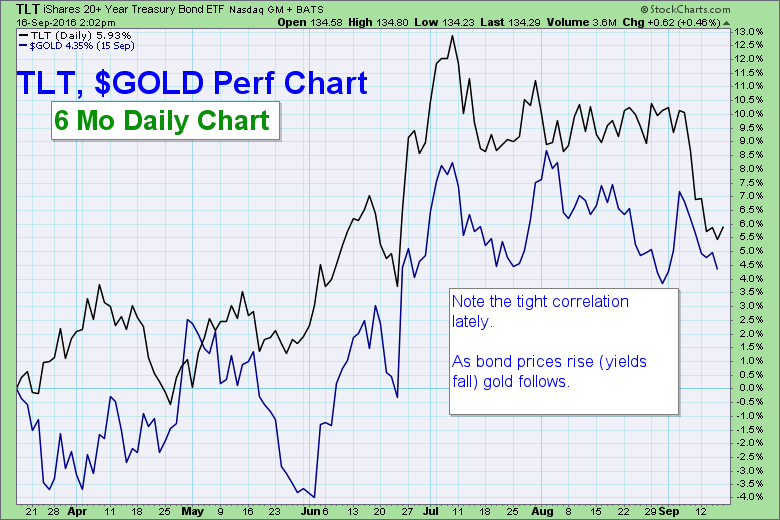

Treasuries vs Gold

While not a “tick-for-tick” 100% correlation, you can clearly see that gold likes low yielding government debt. The global trend towards negative interest rates is a tremendous positive for gold.

Ultimately, this correlation will break as rising rates eventually reveal the rotten balance sheets of the banks and other large institutions. Rates cannot stay artificially suppressed indefinitely.

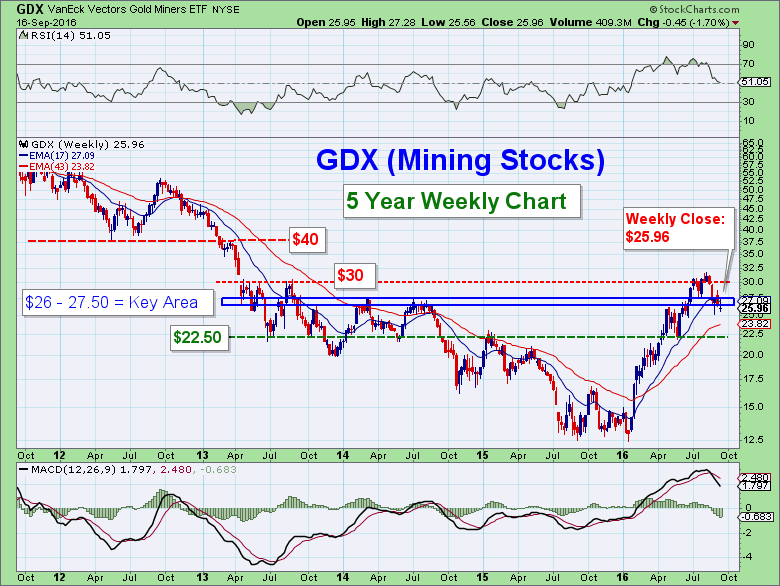

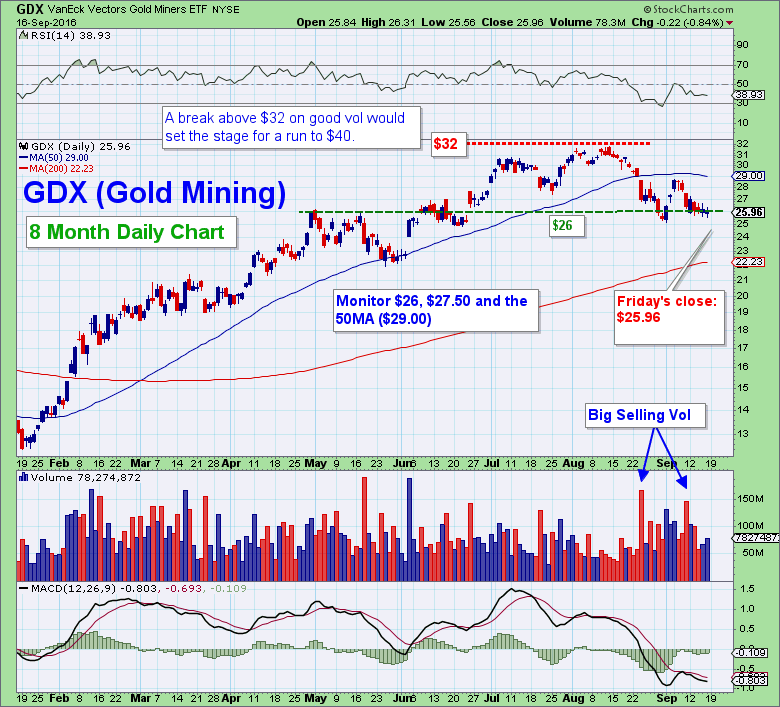

Mining Stocks

The area between $26 and $27.50 is critical for the mining stocks, as clearly seen on the 5-year weekly chart.

$22.50 is strong support and would represent an approximate 50% retracement of the recent rally — not an uncommon occurrence.

Retaking $27.50, and subsequently clearing $30 and $32, represent initial obstacles for the mining stocks.

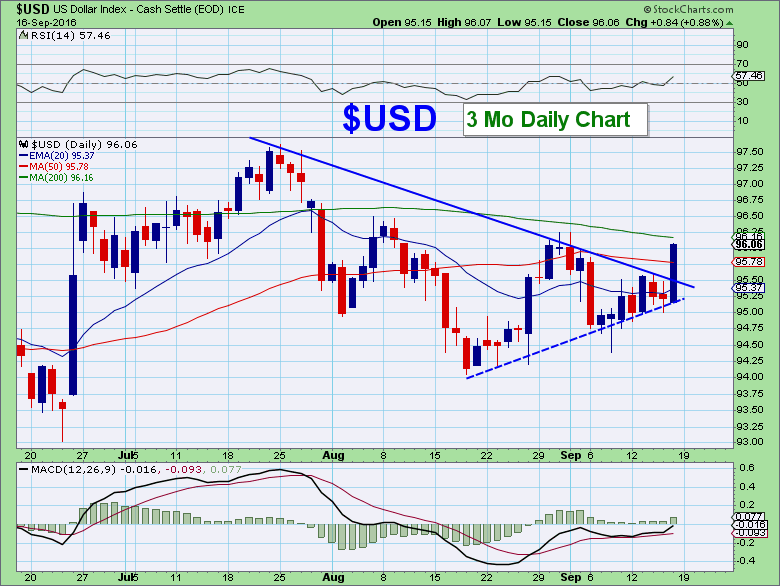

$USD

The dollar broke out of a wedge pattern on Friday, surging to $96.06. The dollar is now above its 20 and 50MAs and just below the 200MA.

At the risk of sounding like a broken record, expectations regarding future interest rate policy will likely determine the near-term direction of the dollar. I really look forward to basing analysis less on the prognostications of a few Fed officials and more on actual fundamental and technical indicators!

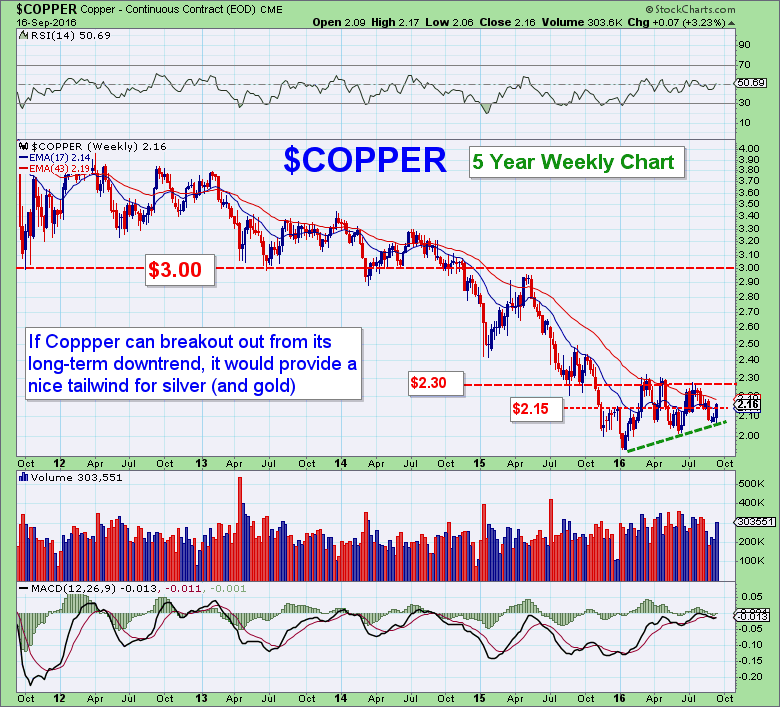

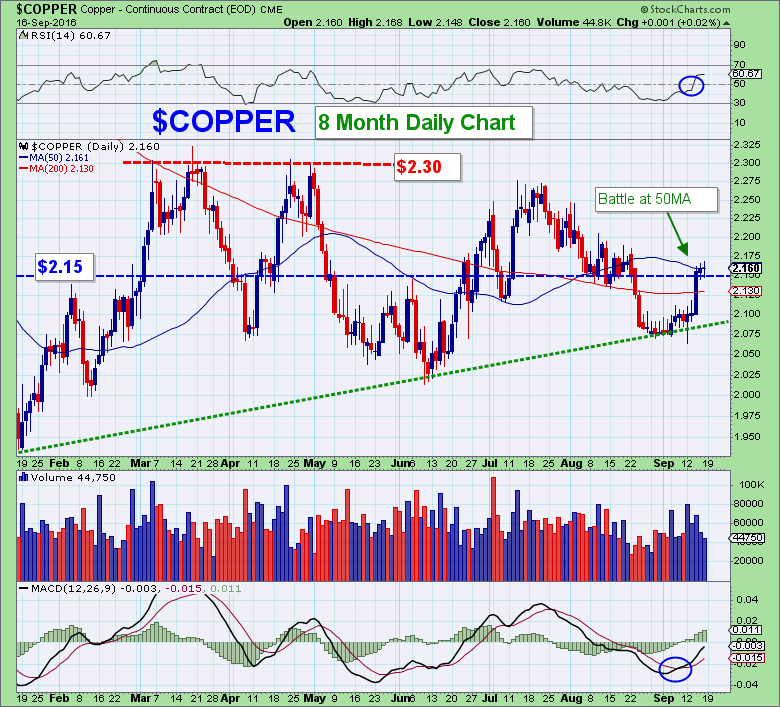

Copper

Copper rallied strongly this week, advancing each of the last five days.

Copper trading above a rising 50 and 200MA bodes well for silver. The last three days of trading have been a battle for copper to retake its 50MA, illustrating the significance of technical analysis. That line clearly matters to big money traders and institutions. Copper closed the week precisely at the 50MA ($2.16.)

While not yet established in a long-term uptrend, copper appears to be carving out a solid base above $2 after a brutal multi-year downtrend.

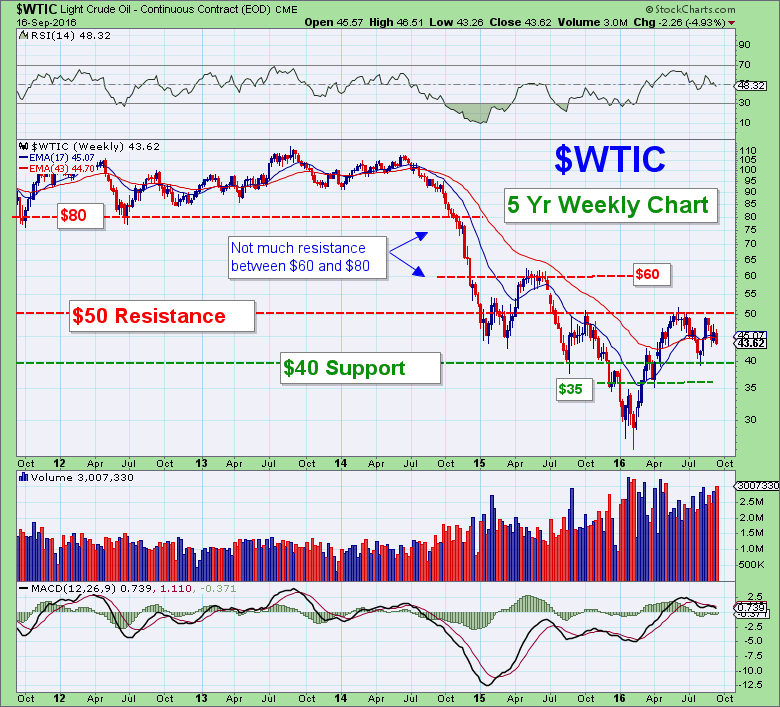

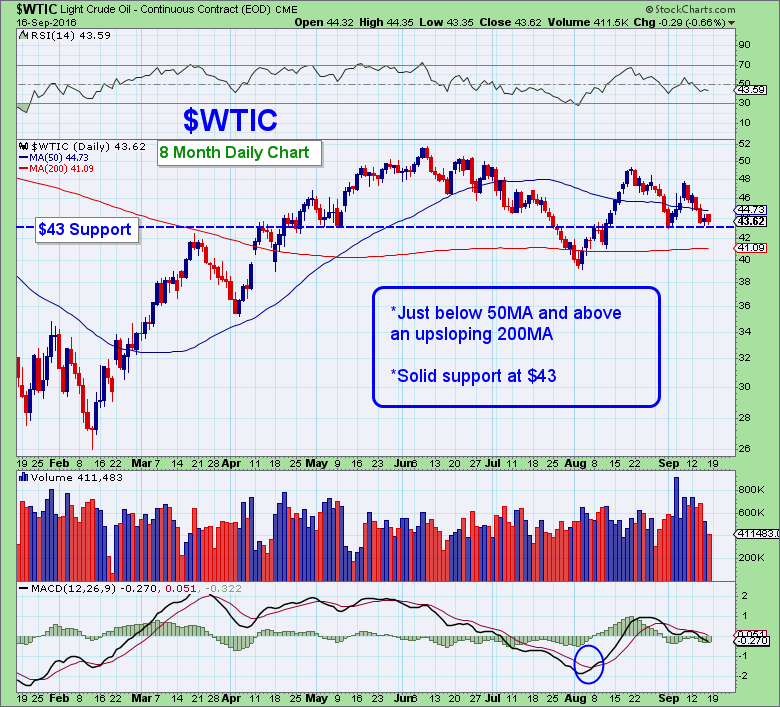

$WTIC

Oil sold off this week, but remains within its $40-$50 trading range and just below its 50MA ($44.73).

There is decent support at $43, just above a rising 200MA ($41.09).

Like copper, a rising oil price would be a positive for the metals–especially silver as both a monetary and industrial metal.

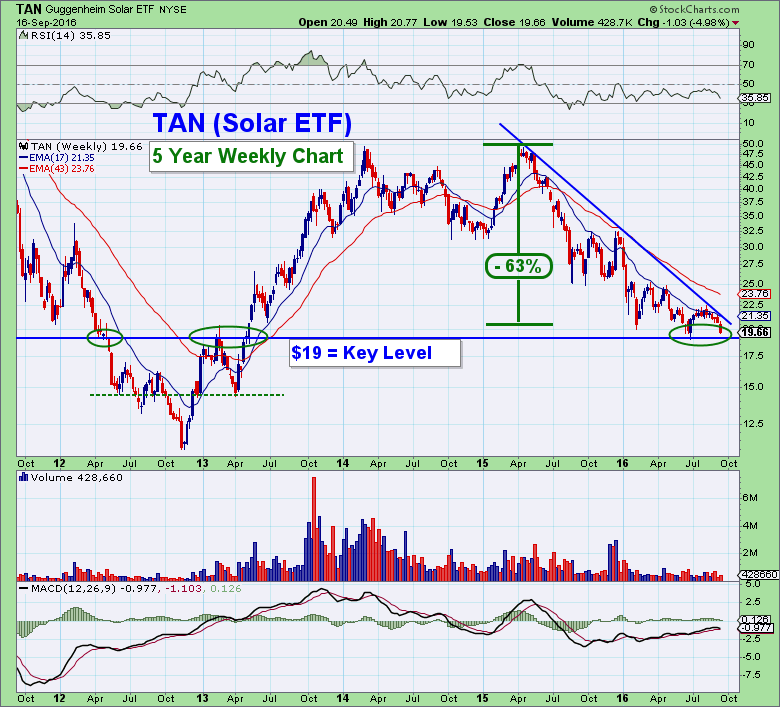

P.A.C.E

*Precious Metals, Agriculture, Commodities, Energy

Each week I’ll highlight one component of the FTM P.A.C.E portfolio. I’ve been monitoring solar, as the TAN Solar ETF may be forming a base near the $19 level, after a 63% decline over the past 18 months.

TAN is working itself towards the apex of a descending triangle pattern that should resolve in the coming weeks. There is speculation that the next “stimulus package” may be global in nature and involve massive infrastructure projects geared heavily towards clean energy. Solar stands to benefit from any such action.

Of course, FTM will be watching for price and volume to confirm a new uptrend before entering. FTM members will be alerted in the Weekend Briefing, as well as the twice-weekly conference calls with Jerry Robinson, should a new uptrend be confirmed.

Commitment of Traders (Big Bank Positioning)

There isn’t much new to report regarding the CoT. While the big banks have covered some of their short positions into the recent decline, they remain positioned heavily short. A sharply lower price is still in their best financial interest. While I don’t like betting against these guys, they have clearly not been able to exert the same influence that they were once able to, and the possibility remains that they will have to cover into a rising price. We’ll see.

Summary

Monitor the key initial support zones at $1300-$1308, $18-18.50 and be on the lookout for the banks to give price a shove in their direction (down) prior to the FOMC and BOJ announcements on Wednesday.

Gold, silver, and the mining stocks are nowhere near oversold and are once again postured in such a way that I am increasingly weary of a quick shove lower to near the $18 and $1250 levels, respectively. We’ll have to see how price and volume respond if $1300 and $18.50 are tested early this week. A high volume bounce off of those levels would alleviate much of the short-term concern. Clearing $19.75 and $1375 would set the stage for the next run higher.

There are plenty of sites out there more than willing to tell you what “they know” will happen in the metals. Be weary of such omniscient claims. It is my sincere belief that FTM’s approach of following trends and not opinions is the best –and most profitable– analysis available and offers incredible value to subscribers.

Have a great week!

God Bless!

Steve Penny

Words to Ponder:

“The last duty of a central banker is to tell the public the truth. “

–Federal Reserve Board Vice Chairman Alan Blinder (retired)

“One man with a gun robs a bank; a few men with banks rob the world”

-Gerald Celente

“When plunder becomes a way of life for a group of men living together in society, they create for themselves in the course of time a legal system that authorizes it & a moral code that glorifies it.” -Frederic Bastiat

PRAISE FOR JERRY 'S BOOK "Jerry Robinson does an excellent job of explaining the 'Petrodollar' system. His book explains exactly how this will come about, but equally important is the comprehensive section on what you can do to protect yourself."

The Strait of Hormuz is one of the most important chokepoints in the global oil market, and now it’s effectively closed in the wake of Washington’s illegal war against Iran. As it turns out, a nation that controls a strategic shipping lane just may close it if...

Topics covered on this special webcast In this live webcast, trading coach Jerry Robinson discusses the importance of analyzing monthly candlestick charts and shares dozens of monthly charts, including Bitcoin, S&P 500, gold, silver, Nvidia, and many more. Plus,...

Topics covered on this special webcast In this live webcast, Jerry Robinson analyzes the Supreme Court’s ruling against the Trump tariffs and its geopolitical and economic implications. He also explores seven key earnings reports to watch this week from stocks in his...

Please help us spread the word about FollowtheMoney.com on Facebook, Twitter, and any other social media outlets.

Silver & Gold

Call 800-247-2812 now for the best prices on gold and silver coins and receive Free Shipping and Insurance when you mention Follow the Money.

Weekly Newsletter

Stay in the loop!

Sign up today to receive our weekly e-newsletter.